Data points to another mortgage boom if rates continue to tumble

Declining mortgage rates and slowing home price appreciation have boosted affordability in many markets and made refinancing a tempting option for 2.5 million homeowners — many of whom are locking rates on refis at levels not seen in more than 2 years.

While that’s good news for mortgage lenders and real estate agents, the latest ICE Mortgage Monitor report from Intercontinental Exchange Inc. also shows the potential for a boom in homebuying and refinancing if mortgage rates keep falling as expected, with the Federal Reserve gearing up this month to shift its stance from fighting inflation to warding off a recession.

Optimal Blue data shows mortgage rates are already down 1.5 percentage points from the post-pandemic high of 7.83 percent registered in October 2023, and affordability is as good as it’s been in six months, ICE’s Andy Walden said.

“Recent easing in mortgage rates brought some much-sought relief to prospective homebuyers,” Walden said in a statement. “Along with a general cooling in home price growth, rates falling below 6.5 percent made August the most affordable month for housing since February.”

Andy Walden

How falling mortgage rates could affect affordability

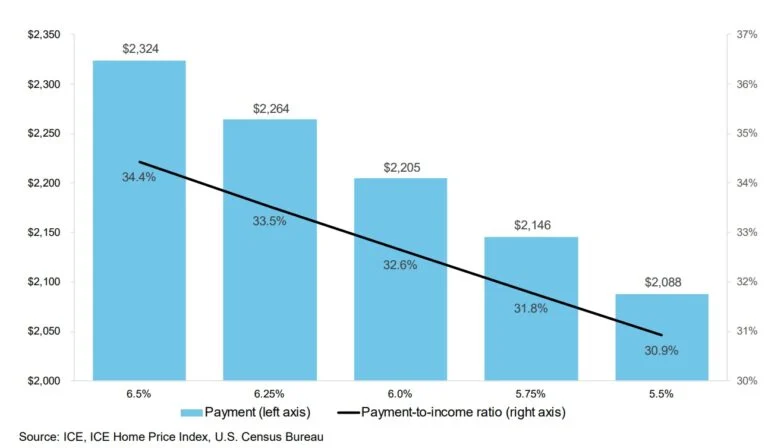

With mortgage rates at 6.5 percent, buying the average home still requires 34 percent of median income — about 10 percentage points higher than the historical average, Walden noted.

Each quarter point mortgage rate reduction reduces the mortgage payment required to purchase the average-priced home by around $60.

So if rates come down another percentage point, to 5.5 percent, payment-to-income ratio drops to 31 percent and homebuyers would be looking at a monthly payment of $2,088 instead of $2,324.

While forecasters at Fannie Mae and the Mortgage Bankers Association expect rates will continue to come down, they don’t anticipate rates on 30-year fixed-rate loans to dip below 6 percent until Q4 2025.

Mortgage rates are only part of the affordability problem. While home prices soared during the pandemic, they are now decelerating and even coming back down in some Sunbelt markets where inventories are growing.

Growing inventory and continuing soft demand slowed annual home price appreciation to 3.6 percent in July, down from 4.1 percent in June, ICE Mortgage estimates.

Looking at the nation’s 100 largest markets, ICE Mortgage sees affordability remaining a challenge in more than half, with the median income needed to make monthly mortgage payments still elevated by 10 percentage points from historical averages.

By that measure (payment-to-income ratio), affordability has returned to historical trendline in seven markets: Birmingham, Alabama; Des Moines, Iowa; McAllen, Texas; Cleveland and Toledo, Ohio; Memphis, Tennessee; and Baton Rouge, Louisiana.

Payment-to-income ratios are within 5 percentage points of historical averages in 22 other markets, ICE Mortgage estimates.

But elevated down payment and tight credit requirements may also be contributing to muted demand, the report warned.

Homebuyers making record down payments

Would-be homebuyers are also facing tight lending requirements, with the average credit score for borrowers taking out purchase loans hitting a record 737 in May, according to ICE Market Trends data.

While homebuyers would welcome lower mortgage rates, they would also benefit recent homebuyers who took out loans when rates were higher.

More homeowners ‘in the money’ for refinancing

As of Aug. 22, 2.5 million homeowners were “in the money” for a refinance, meaning they could save money by refinancing at a lower rate.

Among that group, more than 60 percent took out their mortgages in the past two years, including 850,000 in 2023 and 560,000 this year.

ICE Mortgage calculates that “highly qualified” candidates with credit scores of 720 or higher and at least 20 percent equity in their homes could save $264 a month by refinancing into a new loan that shaves at least 75 basis points off their current rate.

If rates fell by a full percentage point to 5.5 percent, nearly 7.2 million homeowners would be “in the money” for a refinance, and 2.7 million of those would be considered highly qualified, ICE Mortgage estimates.

If rates fell that far, two-thirds of mortgages originated in 2023 and more than 80 percent of loans taken out in 2024 would be in the money for a refinance.

That’s a potential headache for loan servicers who collect monthly mortgage payments for investors, who don’t want their mortgage servicing rights (MSR) portfolios shrink as clients refinance with another lender.

Loan servicers retained only one in five borrowers who refinanced during Q2 2024, down from 25 percent in Q1 and the second lowest retention rate in more than 17 years.

Servicers were “particularly successful in retaining refinancing borrowers who’d recently obtained their loans,” with retention as high as 41 percent among 2023 and 34 percent among 2022 vintage loans, ICE Mortgage noted.

Source: https://www.inman.com/2024/09/04/data-points-to-another-mortgage-boom-if-rates-continue-to-tumble/